English News Headline

Step-Up SIP Strategy Can Help Investors Build Rs 2.73 Crore Corpus in 25 Years

Full Telugu News Article

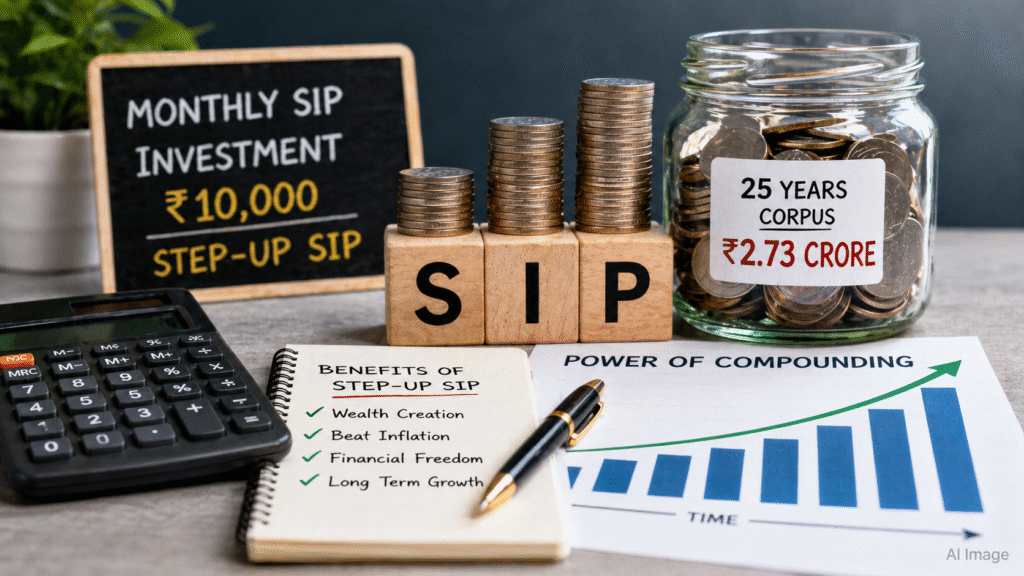

మ్యూచువల్ ఫండ్లలో నెలకు రూ.10 వేల సిప్ పెట్టుబడి పెట్టే వారు చిన్న మార్పు చేస్తే దీర్ఘకాలంలో భారీ లాభం పొందవచ్చని ఆర్థిక నిపుణులు చెబుతున్నారు. సాధారణ సిప్తో పోలిస్తే స్టెప్ అప్ సిప్ ఎంపిక చేసుకుంటే రిటైర్మెంట్ సమయానికి అదనంగా లక్షల రూపాయలు సంపాదించే అవకాశం ఉంటుంది.

సాధారణంగా చాలా మంది ప్రతి నెల ఒకే మొత్తాన్ని సిప్ రూపంలో పెట్టుబడిగా పెడతారు. అయితే ప్రతి సంవత్సరం సిప్ మొత్తాన్ని కనీసం 5 శాతం పెంచుతూ వెళితే కాంపౌండింగ్ ప్రభావం మరింత బలంగా పనిచేస్తుంది. దీనినే స్టెప్ అప్ సిప్ అంటారు.

ఉదాహరణకు 35 ఏళ్ల వయసులో ఇద్దరు మహిళలు సీత, గీత నెలకు రూ.10 వేల చొప్పున మ్యూచువల్ ఫండ్లో సిప్ ప్రారంభించారని భావిద్దాం. వీరిద్దరూ 60 ఏళ్ల వయస్సు వచ్చే వరకు అంటే 25 సంవత్సరాలు పెట్టుబడిని కొనసాగించారు.

ఇక్కడ సీత ప్రతి ఏడాది తన సిప్ మొత్తాన్ని 5 శాతం పెంచుతూ స్టెప్ అప్ సిప్ ఎంచుకుంది. గీత మాత్రం ప్రతి నెలా రూ.10 వేల రెగ్యులర్ సిప్ మాత్రమే కొనసాగించింది.

వార్షికంగా సగటు 12 శాతం రాబడి ప్రాతిపదికగా చూస్తే, సీతకు 25 ఏళ్ల తర్వాత రూ.2.73 కోట్ల కార్పస్ ఏర్పడింది. అదే గీతకు రూ.1.90 కోట్లు మాత్రమే లభించాయి.

పెట్టుబడి పరంగా గీత మొత్తం 25 ఏళ్లలో రూ.30 లక్షలు మాత్రమే పెట్టుబడి పెట్టింది. సీత మాత్రం స్టెప్ అప్ కారణంగా మొత్తం రూ.57.27 లక్షలు పెట్టుబడి పెట్టింది. అంటే అదనంగా రూ.27.27 లక్షలు మాత్రమే పెట్టి, చివరికి రూ.83 లక్షల అదనపు రాబడి పొందింది.

ఆర్థిక నిపుణుల అభిప్రాయం ప్రకారం ప్రతి ఏడాది జీతం పెరుగుదల లేదా బోనస్ వచ్చినప్పుడు సిప్ మొత్తాన్ని కొద్దిగా పెంచడం పెద్ద భారంగా ఉండదు. దీర్ఘకాలిక ఆర్థిక లక్ష్యాల కోసం ఇది మంచి వ్యూహంగా మారుతుంది.

అయితే మ్యూచువల్ ఫండ్ పెట్టుబడులు మార్కెట్ రిస్క్కు లోబడి ఉంటాయి. అందువల్ల పెట్టుబడి పెట్టే ముందు సెబీ గుర్తింపు పొందిన ఆర్థిక నిపుణుల సలహా తీసుకోవడం మంచిదని సూచిస్తున్నారు.

Full English News Article

Investors putting Rs 10,000 every month in mutual fund SIPs can significantly increase their long-term wealth by following a simple step-up strategy, according to financial experts. Compared to regular SIP investing, Step-Up SIP can generate a much larger retirement corpus over time.

In a regular SIP, investors continue investing the same amount every month for years. However, in Step-Up SIP, the monthly investment amount is increased every year, usually by 5 to 10 percent, depending on salary growth and financial capacity.

For example, if two investors, Sita and Geetha, both start investing Rs 10,000 per month at the age of 35 and continue until retirement at 60, the final corpus can vary significantly depending on the strategy chosen.

Sita selects the Step-Up SIP option and increases her SIP amount by 5 percent every year. Geetha continues with a regular SIP of Rs 10,000 every month without any increase.

Assuming an average annual return of 12 percent, Sita builds a retirement corpus of Rs 2.73 crore in 25 years. Geetha, on the other hand, accumulates Rs 1.90 crore during the same period.

In terms of total investment, Geetha invests Rs 30 lakh over 25 years. Sita invests Rs 57.27 lakh because of the yearly increase. Though Sita invests Rs 27.27 lakh more, she gains an additional Rs 83 lakh in final returns.

Financial planners say increasing SIP contributions slightly every year is not difficult, especially when income grows annually. This helps investors fight inflation and create a stronger financial cushion for the future.

However, mutual fund investments are subject to market risks. Experts advise investors to consult SEBI-registered financial advisors before making investment decisions based on their risk profile and long-term goals.