English News Headline

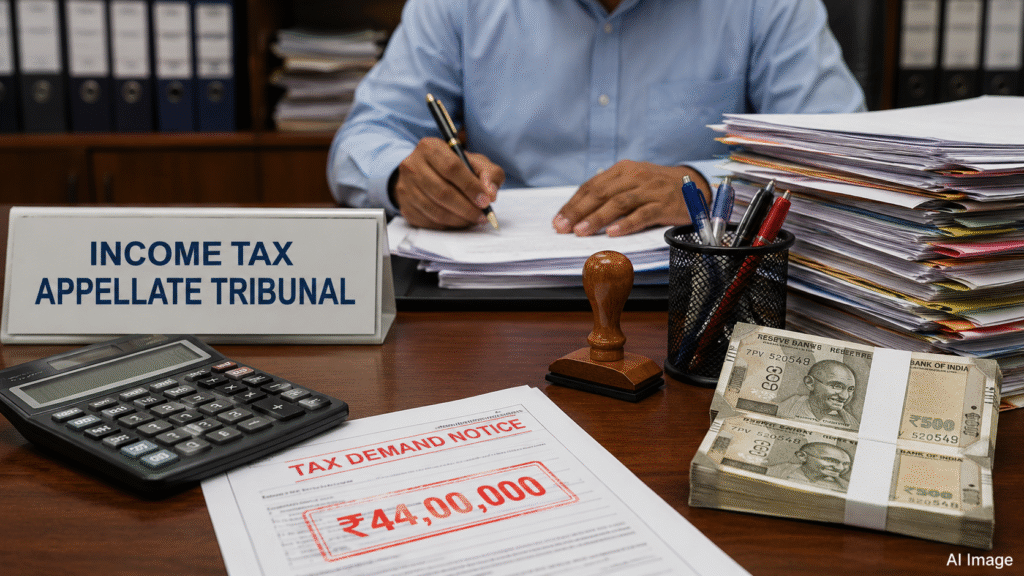

ITAT Relief for Scrap Dealer After ₹44 Lakh Tax Demand Over Cash Deposits

Full Telugu News Article

తన వార్షిక ఆదాయం కేవలం రూ.3 లక్షలేనని ఆదాయపు పన్ను రిటర్నుల్లో ప్రకటించిన ఓ స్క్రాప్ వ్యాపారికి రూ.44 లక్షల పన్ను డిమాండ్ నోటీసులు జారీ కావడం చర్చనీయాంశంగా మారింది. అయితే చివరకు ఆదాయపు పన్ను అప్పిలేట్ ట్రైబ్యునల్ (ITAT) జోక్యంతో ఆ వ్యాపారికి ఊరట లభించింది.

వజీద్ ఖాన్ అనే స్క్రాప్ వ్యాపారి 2015-16 ఆర్థిక సంవత్సరానికి సంబంధించి రూ.3,00,340 ఆదాయాన్ని ప్రకటించారు. అయితే ఆయన సహకార బ్యాంకు ఖాతాలో రూ.1.28 కోట్ల నగదు డిపాజిట్లు నమోదైనట్లు ఆదాయపు పన్ను శాఖ గుర్తించింది.

ఆదాయం మరియు బ్యాంకు డిపాజిట్ల మధ్య భారీ వ్యత్యాసం ఉండటంతో ఐటీ అధికారులు సెక్షన్ 147 కింద కేసును తిరిగి తెరిచి విచారణ చేపట్టారు. అనంతరం రూ.1.28 కోట్లను అన్ఎక్స్ప్లెయిన్డ్ మనీగా పరిగణించి సెక్షన్ 115BBE కింద దాదాపు రూ.44 లక్షల పన్ను డిమాండ్ విధించారు.

తన వ్యాపారం పూర్తిగా నగదు లావాదేవీల ఆధారంగా సాగుతుందని, టర్నోవర్పై 8 శాతం లాభాన్ని మాత్రమే పరిగణనలోకి తీసుకోవాలని వజీద్ ఖాన్ వాదించారు. అయితే కంప్యూటర్ డేటా వైరస్ కారణంగా దెబ్బతినడంతో పూర్తి రికార్డులు సమర్పించలేకపోయినట్లు తెలిపారు.

కేసు ఐటీఏటీ ముందు విచారణకు రాగా, గత మరియు తదుపరి సంవత్సరాల్లో ఇదే వ్యాపార విధానాన్ని ఆదాయపు పన్ను శాఖ ఆమోదించిన విషయాన్ని ట్రైబ్యునల్ పరిగణనలోకి తీసుకుంది. ‘ప్రిన్సిపల్ ఆఫ్ కన్సిస్టెన్సీ’ ఆధారంగా ఒకే వ్యాపార విధానాన్ని ఒక్క సంవత్సరంలో మాత్రమే తిరస్కరించడం సరైన విధానం కాదని అభిప్రాయపడింది.

దీంతో రూ.44 లక్షల పన్ను డిమాండ్ ఆర్డర్ను రద్దు చేసిన ట్రైబ్యునల్, కేసును తిరిగి అసెస్సింగ్ అధికారికి పంపిస్తూ గత సంవత్సరాల లాభాల అంచనా విధానం ప్రకారమే పన్ను లెక్కించాలని ఆదేశించింది.

పూర్తి నగదు లావాదేవీలతో వ్యాపారాలు నిర్వహించే చిన్న వ్యాపారులకు ఈ తీర్పు ఉపశమనం కలిగించే అవకాశముంది. అయితే వ్యాపార రికార్డులు, బ్యాంకు స్టేట్మెంట్లు, జీఎస్టీ పత్రాలు, ఖాతా పుస్తకాలను భద్రంగా ఉంచుకోవడం అవసరమని పన్ను నిపుణులు సూచిస్తున్నారు.

Full English News Article

A scrap dealer who declared an annual income of just ₹3 lakh in his income tax return received a tax demand notice of nearly ₹44 lakh after authorities found cash deposits worth ₹1.28 crore in his bank account. However, the Income Tax Appellate Tribunal (ITAT) later provided significant relief in the case.

The taxpayer, Wajid Khan, a scrap trader, reported an income of ₹3,00,340 for the financial year 2015-16. During scrutiny, the Income Tax Department identified cash deposits totaling ₹1.28 crore in his cooperative bank account through its data analytics system.

Citing a substantial mismatch between declared income and bank deposits, tax authorities reopened the assessment under Section 147 of the Income Tax Act. The deposits were treated as unexplained money, and a tax demand of around ₹44 lakh was raised under Section 115BBE.

Khan argued that his scrap business primarily operated through cash transactions and sought taxation under the presumptive taxation provisions, which estimate profit at a fixed percentage of turnover. He also stated that accounting records had been lost due to a computer virus.

When the matter reached the ITAT, the tribunal examined previous and subsequent assessment records and noted that the Income Tax Department had accepted the same business model and profit estimation method in other years.

Invoking the principle of consistency, the tribunal observed that authorities could not reject the same accounting approach for one year alone without adequate justification. It subsequently set aside the ₹44 lakh tax demand and directed the Assessing Officer to reconsider the case based on past assessment practices.

The ruling is expected to provide guidance for small businesses dealing largely in cash transactions, while highlighting the importance of maintaining proper financial records and documentation.